Recently, many institutions have shared their predictions for the future of the semiconductor industry. Below, we have compiled some recently released reports on semiconductor industry forecasts to help you make some decisions about the future of semiconductors. Before sharing industry data, let's take a look at which field uses the most chips.

Over the past few decades, semiconductors have become ubiquitous not only in devices such as smartphones, computers, or home appliances but also in manufacturing, for example in cars or industrial robots. But which industries account for the largest share of semiconductor purchases?

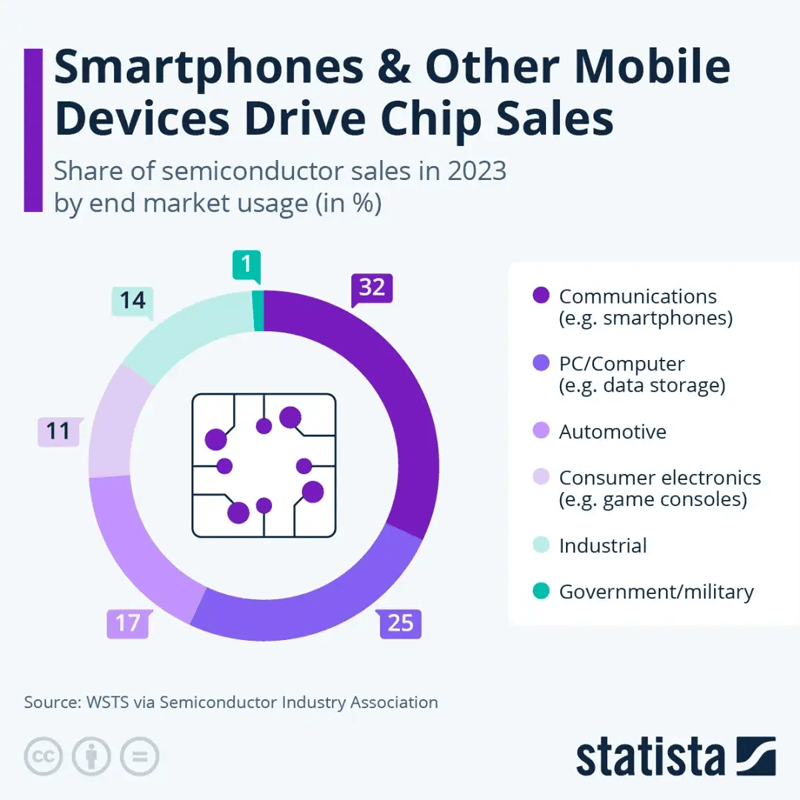

According to the 2024 overview data of the Semiconductor Industry Association (SIA), a US lobbying group, most chips purchased in 2023 were used in the PC and communications sectors. The former includes everything from computer memory to chips used in data centers, while the latter covers smartphones, tablets, and other wireless and wired communication devices. 57% of the estimated $527 billion in semiconductor sales come from these two industries. Automotive and industrial accounted for 17% and 14% respectively, while consumer electronics accounted for 11% of the entire semiconductor market in the past year.

SIA also believes that the US semiconductor industry accounts for 50.2% of the revenue market share, although this number needs to be examined carefully. For example, Nvidia is a US-based semiconductor company, but its chips are produced by TSMC, the world's leading semiconductor foundry in Taiwan. So while US companies may make the most money from chip sales, most of the actual production is done elsewhere. 70% of 300mm wafers (considered the current industry standard in terms of efficiency) are made in South Korea, Taiwan, China, and China.

Below, we look at industry forecasts. It should be emphasized that these institutional data are for reference only and do not represent the full facts or our opinions.

SEMI estimates that semiconductors will grow by 20%

For example, the Semiconductor Industry Association (SEMI) estimates that global semiconductor revenue is expected to grow by 20% this year, with artificial intelligence (AI) chips and storage being the main growth drivers. Next year, as demand for communications, industrial and automotive applications recovers, semiconductor revenue will grow another 20%.

SEMI Senior Director of Industry Research Zeng Ruiyu analyzed the development trend of the global semiconductor market at the SEMI conference held in Taiwan, China yesterday.

Zeng Ruiyu pointed out that electronic equipment sales in the first half of this year were about the same as the same period last year, and the third quarter is expected to increase by 4% year-on-year, and the annual increase will be 3%~5%, slightly lower than the original estimate of 5%~7%. Semiconductor revenue grew by more than 20% in the first half of this year compared with the same period last year. Zeng Ruiyu expects that semiconductor revenue this year is expected to grow by 20%. In addition to the rise in memory prices and volumes, AI chips are also the main growth drivers.

Zeng Ruiyu said that semiconductor revenue excluding memory will grow by about 10% this year. If AI-related chip products are excluded, semiconductor revenue this year will only grow by 3%. Zeng Ruiyu said that as supply chain inventories in communications, industry and automotive applications are approaching the bottom, demand is expected to recover healthily next year, and semiconductor revenue will have the opportunity to grow by 20% next year.

He pointed out that the capacity utilization rate of wafer fabs hit the bottom in the first quarter of this year and began to gradually recover in the second quarter. It is expected that the capacity utilization rate in the third quarter will reach 70%, and further recovery will occur in the fourth quarter.

Zeng Ruiyu said that the investment amount in mainland China in the first half of this year surged by 90% compared with the same period last year. The main reason behind this is that the United States is worried about stricter regulations and actively builds sufficient mature process capacity; the investment in other countries and regions in the first half of the year mostly decreased compared with the same period last year. Zeng Ruiyu estimates that due to the large-scale investment by mainland China based on geopolitical factors, the global semiconductor equipment market this year is expected to grow slightly by 3% to US$109.5 billion compared with last year. Next year, driven by advanced logic chips and packaging and testing, the equipment market will grow by 16% compared with this year to US$127.5 billion.

He said that the annual compound growth rate of semiconductor equipment spending in the United States from 2023 to 2027 is expected to reach 22%, the annual compound growth rate in Europe and the Middle East is 19%, Japan is 18%, South Korea is 13%, Taiwan is about 9%, and mainland China may show negative growth.

Multiple institutions, strong chip market

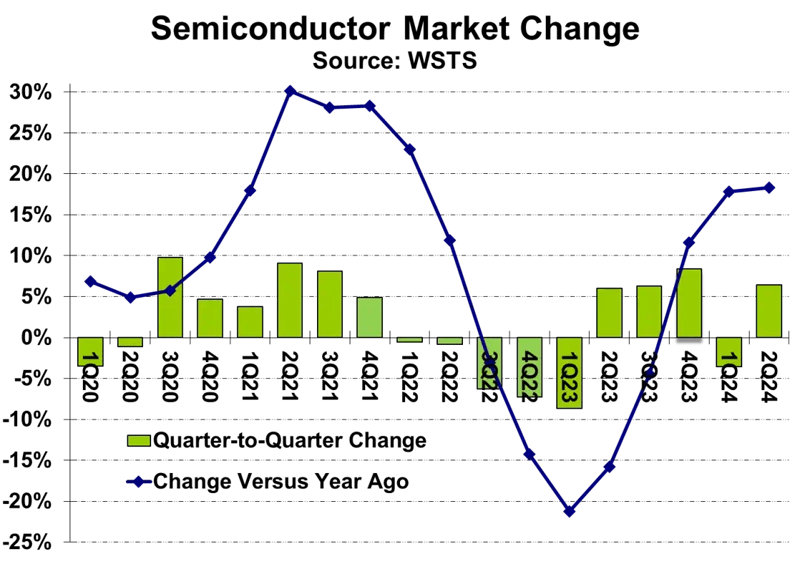

According to WSTS, the global semiconductor market size will reach $149.9 billion in the second quarter of 2024. The second quarter of 2024 will increase by 6.5% from the first quarter of 2024 and increase by 18.3% from the same period last year. WSTS raised its forecast for the first quarter of 2024 by $3 billion, making the first quarter of 2024 increase by 17.8% from the same period last year, instead of the previous 15.3%.

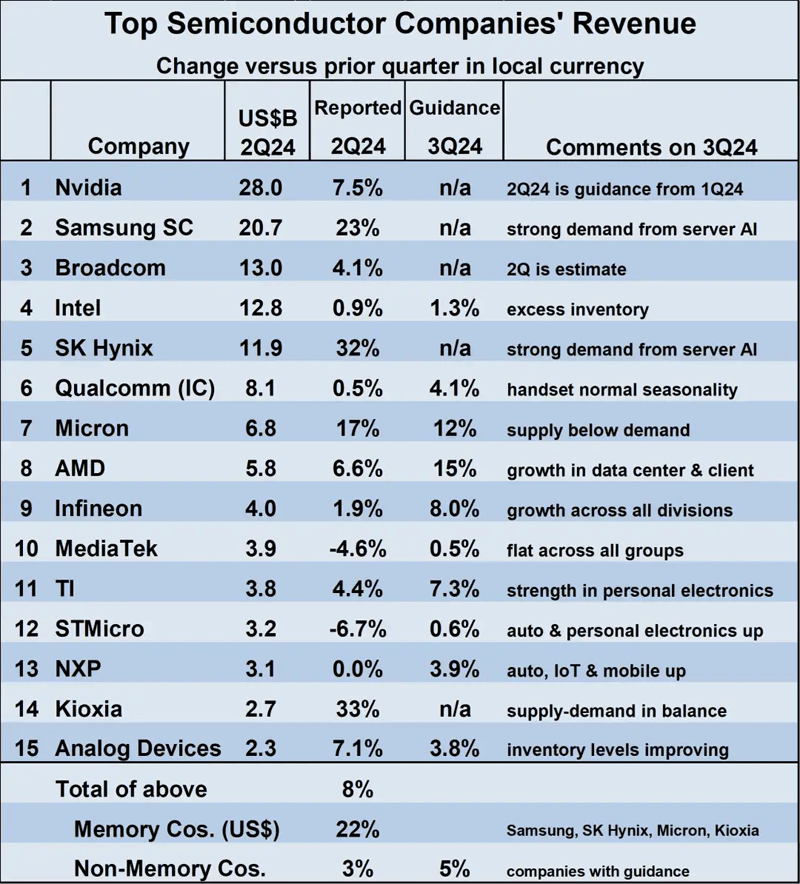

Revenue growth for major semiconductor companies was generally strong in Q2 2024 compared to Q1 2024. Only two of the top fifteen companies (MediaTek and STMicroelectronics) saw revenue declines in Q2 2024. The strongest growth was among memory companies, with SK Hynix and Kioxia up more than 30% each, Samsung Semiconductor up 23%, and Micron Technology up 17%. The weighted average growth rate for the top fifteen companies in Q2 2024 compared to Q1 2024 was 8%, with memory companies up 22% and non-memory companies up 3%.

Nvidia remains the largest semiconductor company based on its Q1 2024 forecast of $28 billion in Q2 2024 revenue (actual revenue reached a record $30 billion). Samsung is second with $20.7 billion. Broadcom has not yet announced its Q2 2024 results, but we estimate its revenue to be $13 billion, surpassing Intel's $12.8 billion. Intel, which for many years ranked first or second, slipped to fourth place this year.

Revenue guidance for the third quarter of 2024 compared to the second quarter of 2024 is positive but broad. AMD expects revenue to grow 15% in the third quarter of 2024, driven by strong growth in data centers and client computing. Micron said the memory boom will continue with supply below demand and expects growth of 12%. Samsung Semiconductor and SK Hynix did not provide revenue guidance, but both companies expect continued strong demand for server AI.

A few companies expect lower revenue growth in the third quarter of 2024, about 1%: Intel, MediaTek, and STMicroelectronics. Intel blames excess inventory for the weak outlook. The other five companies that provided revenue guidance have revenue growth rates between 4% and 8%. STMicroelectronics and NXP Semiconductors expect the automotive industry to improve in the third quarter of 2024, but inventory issues in the industrial sector remain. Texas Instruments expects strong performance in personal electronics. The weighted average revenue growth rate for the third quarter of 2024 for the nine non-memory companies that provided guidance is 5%.

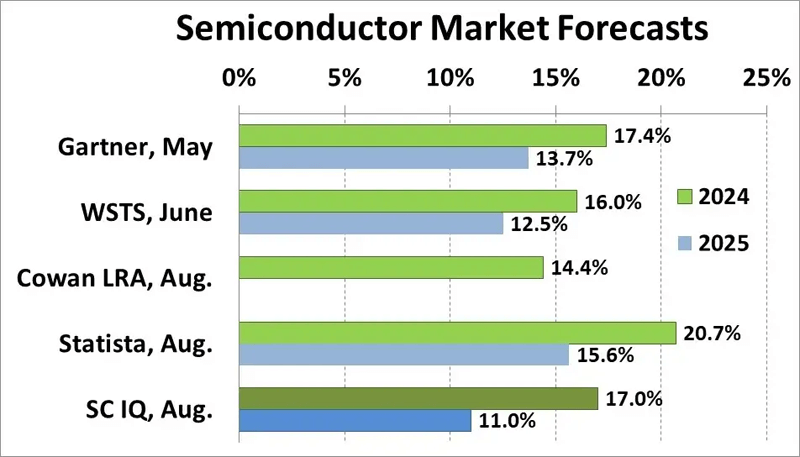

Substantial semiconductor market growth in the first half of 2024 (up 18% from the first half of 2023) will drive strong full-year growth in 2024. Forecasts for 2024 over the past few months have ranged from 14.4% from the Cowan LRA model to 20.7% from Statista Market Insights. Our Semiconductor Intelligence (SC-IQ) forecast for 2024 is 17.0%, in line with Gartner’s 17.4% and WSTS’ 16.0%.

The four forecasts for 2025 show similar trends—slower but still strong growth, ranging from 11.0% by Semiconductor Intelligence to 15.6% by Statista. The deceleration in growth from 2024 to 2025 ranges from minus 3.5 percentage points (16% to 12.5%) by WSTS to minus 6 percentage points (17% to 11%) by ours.

Our preliminary forecast for 2026 is in the mid-single digits. By then, the recovery in the AI and memory markets should taper off. Other major end markets (smartphones, PCs, and automotive) are likely to remain flat or have low growth over the next few years. Barring any major new growth drivers that boost the market or a recession that dampens it, the outlook for the semiconductor market should remain in the mid-single digits through the end of the decade.

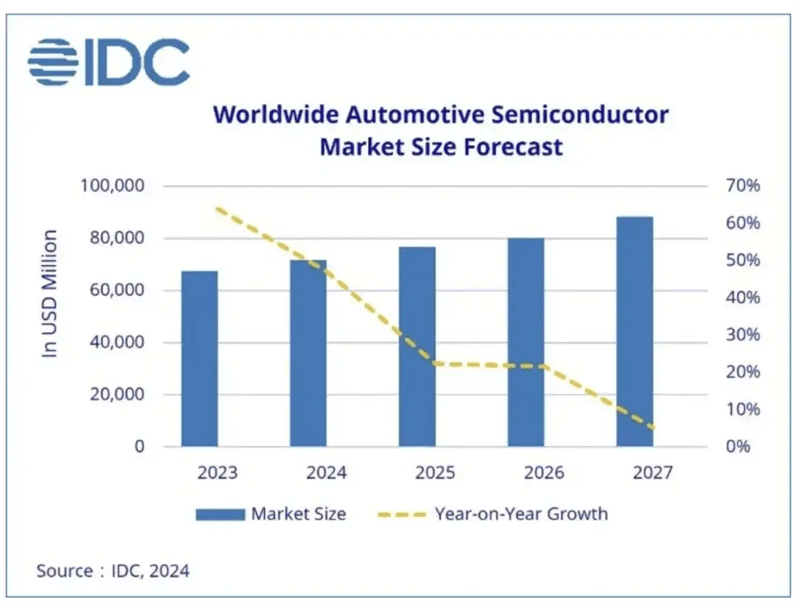

Automotive chips, $88 billion

According to IDC, the global automotive semiconductor market is expected to exceed $88 billion by 2027, driven by surging demand for high-performance computing (HPC) chips, graphics processing units (GPUs), radar chips, and laser sensors. This growth is driven by the increasing popularity of advanced driver assistance systems (ADAS), electric vehicles (EVs), and the Internet of Vehicles (IoV), bringing new growth opportunities to the automotive semiconductor industry, according to a recent report released by International Data Corporation (IDC) titled "Global Automotive Semiconductor Competition Landscape 2023".

IDC predicts that as the value of semiconductors per car continues to rise, semiconductor companies will become increasingly important to the automotive supply chain.

Leading semiconductor companies such as Infineon, NXP, STMicroelectronics, Texas Instruments (TI), and Renesas Electronics are investing heavily in the development of next-generation microcontrollers, system-on-chip (SoC), and high-resolution radar solutions. To meet the automotive demand for greater capacity, higher performance, and higher safety of semiconductors, they continue to enhance ADAS, autonomous driving systems, cockpit and network functions, and integrate complex electronic control units (ECUs) and sensor fusion technologies.

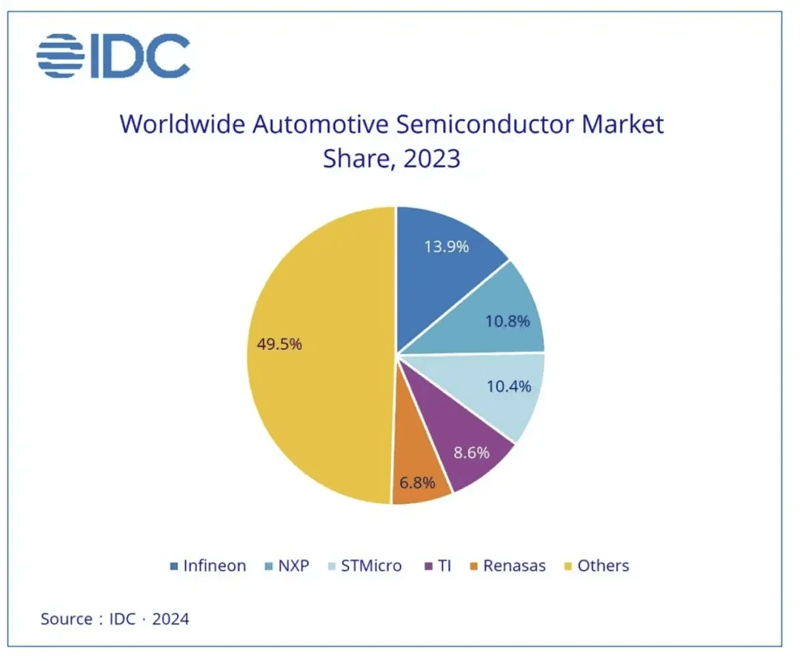

According to the latest report released by IDC, the market share of the top five manufacturers in the automotive semiconductor market will exceed 50% in 2023. Among them, Infineon ranks first with a share of 13.9%; followed by NXP and STMicroelectronics, with market shares of 10.8% and 10.4% respectively; Texas Instruments and Renesas Electronics also performed very well, accounting for 8.6% and 6.8% of the total share respectively. The market structure is as follows:

● Through continuous technological innovation, strategic acquisitions, a sound supply system, and close cooperation with automotive original equipment manufacturers (OEMs), Infineon has continuously improved its market position in power electronics and advanced control systems and established its leadership in the power semiconductor market.

● NXP has a deep accumulation of vehicle-to-everything (V2X) communication and safety technology and continues to innovate and iterate. Through close cooperation with automotive OEMs and Tier 1 suppliers, it provides comprehensive product solutions and is a leader in this field.

● STMicroelectronics provides innovative solutions for the automotive industry with its professional experience in microelectromechanical systems (MEMS) and power semiconductors.

● TI has a rich portfolio of analog chips and embedded solutions, providing a product portfolio that meets customer needs, and has a strong supply chain management and product quality management system as support.

● Renesas Electronics provides a comprehensive range of microprocessors and SoC products to ensure functional safety and reliability while maintaining its industry leadership through strategic acquisitions and cooperation.

Advances in the automotive industry have driven the demand for high-performance, high-safety semiconductors. As electric vehicles and autonomous driving technologies develop, these semiconductor companies will continue to play a key role in the global automotive semiconductor market.

Adela Guo, research director of IDC Asia Pacific, said: "The common advantages of these leading semiconductor suppliers include strong R&D investment and strong technology leadership, a comprehensive product portfolio, solid strategic partnerships, efficient global operations, and safe and reliable product performance. These characteristics enable them to maintain their competitive advantage and drive the sustainable development of the automotive industry towards electrification, networking, and intelligence."

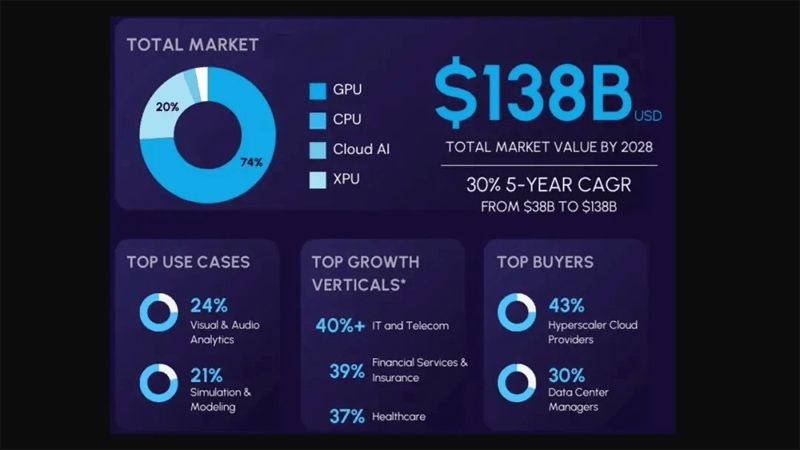

Astonishing demand for AI chips has catapulted Nvidia into a deep-pocketed company over the past year, and that trend is set to continue, according to a recent AI chipset market forecast from research firm Futurum Group. They predict that the global market value for processors and accelerators used for AI applications in the data center market will soar from $38 billion last year to $138 billion in 2028, a compound annual growth rate (CAGR) of 30%.

Of course, this is great news for Nvidia, which is currently the clear market leader in AI chips: it can’t currently keep up with demand for its graphics processing units (GPUs). In 2023, GPU sales for datacenter AI deployments are $28 billion (74% of the total market), with Nvidia accounting for 92% of the segment. But there’s even better news to come, as the value of this particular segment is expected to grow at a compound annual growth rate (CAGR) of 30% over the next five years, reaching $102 billion by 2028.

But as the Futurum team points out, GPUs aren’t the only thing that matters: GPU sales account for 74% of the total value of the data center AI chip market in 2023, but CPUs (central processing units) account for about 20% or $7.7 billion of the $38 billion total. CPUs will continue to play an important role, with the segment growing to $26 billion by 2028.

While Nvidia is currently the leader in the segment, it faces challenges. "We are witnessing the most profound technological revolution with the advent of artificial intelligence and its supporting semiconductor solutions," said David Newman, CEO of Futurum Group. "Companies such as Nvidia, AMD, and Arm are seeing significant revenue growth as AI innovations advance, but the competitive landscape is expected to intensify as new entrants and startups prepare to capture market share and drive continued innovation."

The report notes that a large portion of the demand for AI application processors and accelerators in the data center market comes from hyperscale cloud services companies such as Amazon Web Services (AWS), Google, Microsoft, and Oracle - which together account for 43% of the market value in 2023, and the Futurum team expects this proportion to rise to 50% by 2028. (However, the team noted that processors and accelerators designed for AI applications by companies such as Apple, Meta, and Tesla were excluded from its research because they are only used for private data center processing.)

The Futurum team also pointed out further that the market value of the AI chip industry exceeds $5 trillion, accounting for about 30% of the weight of the S&P 500 index, which is a market capitalization-weighted indicator of the 500 leading public companies in the United States: while it is not an accurate reflection of the top 500 companies, it has a reputation as one of the best indicators of the performance of not only well-known American companies but also the performance of the entire stock market.

The Futurum report shows that currently, the largest use case for AI chipsets is to enable visual and audio analysis (24%), followed by simulation and modeling (21%). The fastest-growing use cases are object recognition, detection, and monitoring, followed closely by conversational AI.